| Chapter 1 Who is Hindu? Chapter 2 Hindu Undivided Family (Concept and Creation) Chapter 3 Coparcener Chapter 4 Karta Chapter 5 HUF and Property Chapter 6 Partition Chapter 7 Family Arrangement Chapter 8 HUF and Business Chapter 9 Residential Status of HUF and Taxability Chapter 10 HUF and Taxation Chapter 11 Assessment of Hindu Undivided Family Chapter 12 Tax Deduction at Source Chapter 13 Hindu Succession Chapter 14 Hindu Marriages Chapter 15 Adoption and Maintenance Chapter 16 Minority and Guardianship Chapter 17 Frequently Asked Questions Appendix 1 Rates of Tax Appendix 2 Return Forms with ITR V/Acknowledgment ITR-2 For Individuals and HUFs not having income from profits and gains of business or profession ITR-3 For individuals and HUFs having income from profits and gains of business or profession ITR-4 SUGAM: For Individuals, HUFs and Firms (other than LLP) being a resident having total income upto Rs. 50 lakh and having income from business and profession which is computed under sections 44AD, 44ADA or 44AE ITR-V Where the data of the Return of Income in Forms ITR-2, ITR-3, SUGAM (ITR-4) filed but NOT verified electronically Acknowledgement Where the data of the Return of Income in Form ITR-2, ITR-3, SUGAM (ITR-4) filed and verified |

Sale!

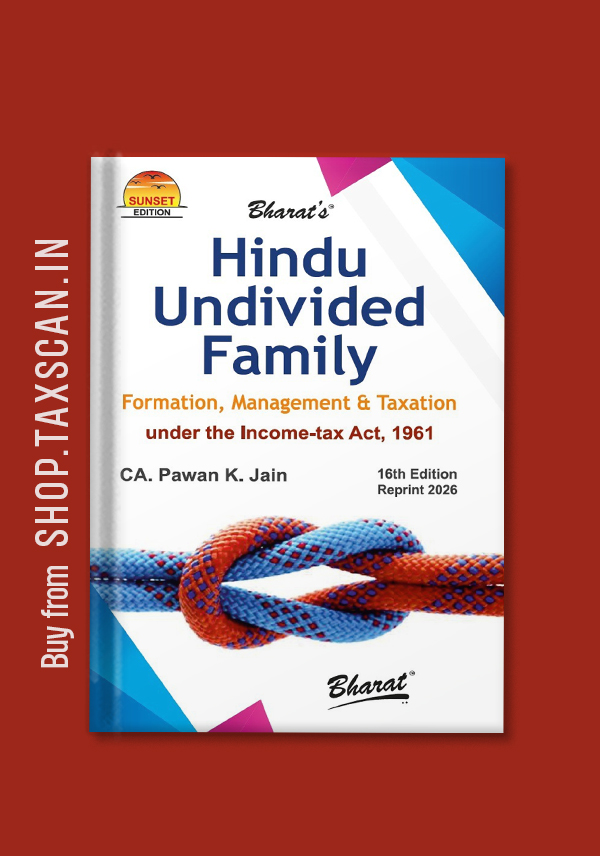

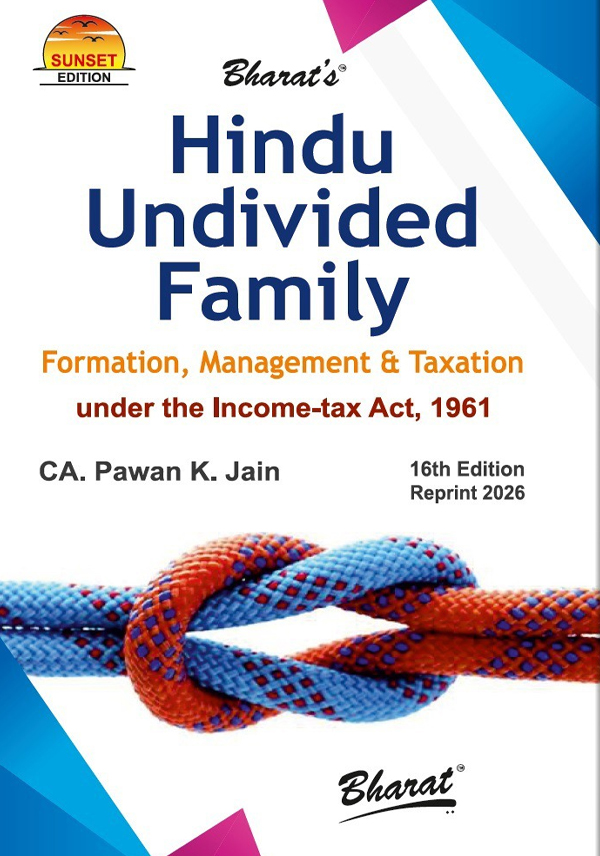

Hindu Undivided Family (Formation, Management & Taxation)

Original price was: ₹1,435.00.₹1,062.00Current price is: ₹1,062.00. Save 26%

Related products

- Sale!

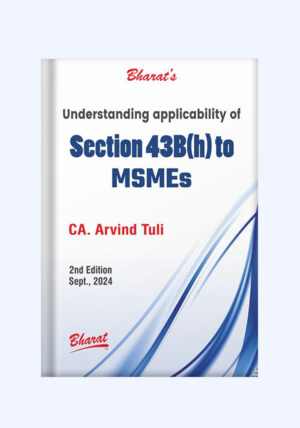

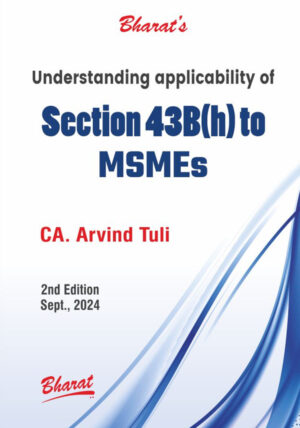

Understanding Applicability of Section 43b(h) to MSMEs

Books Original price was: ₹395.00.₹336.00Current price is: ₹336.00. Save 15%Add to cart - Sale!

Winding Up of Companies (Law, Accounting & Taxation)

Books Original price was: ₹995.00.₹747.00Current price is: ₹747.00. Save 25%Add to cart - Sale!

Treatise on Schedule III (A guide for preparation of Financial Statements)

Books Original price was: ₹1,195.00.₹897.00Current price is: ₹897.00. Save 25%Add to cart - Sale!

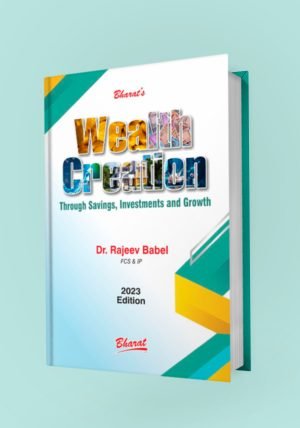

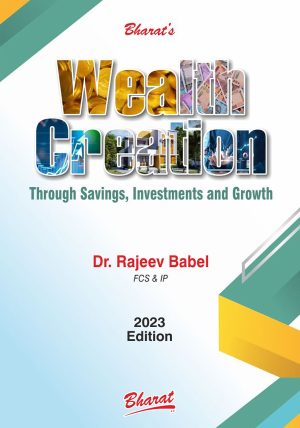

Wealth Creation Through Savings, Investments and Growth

Books Original price was: ₹1,995.00.₹1,696.00Current price is: ₹1,696.00. Save 15%Add to cart

Reviews

There are no reviews yet.