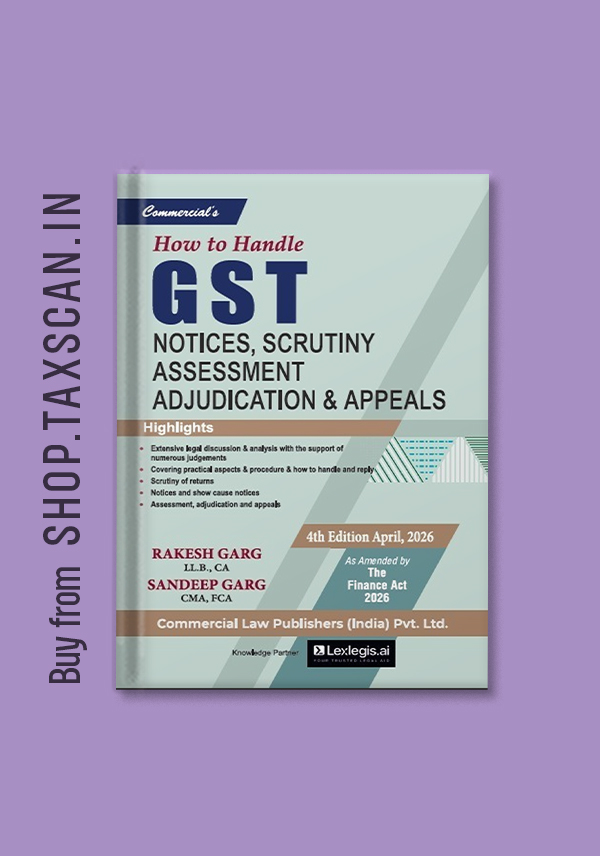

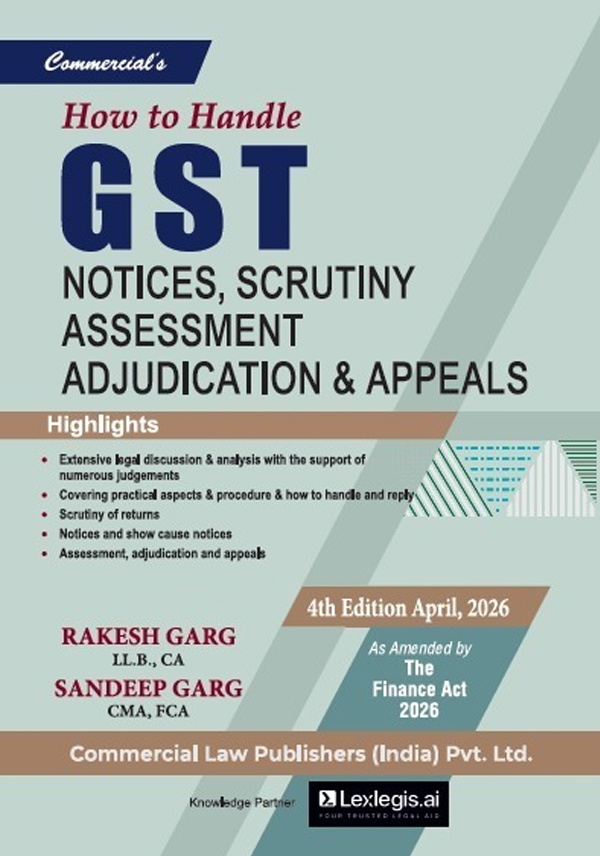

- This edition of How to Handle GST Notices, Scrutiny, Assessment, Adjudication & Appeals, 4th Edition (April 2026), authored by Rakesh Garg and Sandeep Garg, and updated in accordance with the Finance Act, 2026, serves as a comprehensive and practical guide for navigating the complexities of GST litigation and compliance procedures. Designed for professionals, practitioners, and students, the book provides in-depth legal analysis supported by relevant judicial pronouncements, while maintaining a clear focus on real-world application and procedural clarity.

- The book offers a structured and detailed understanding of the processes involved in handling GST notices and departmental actions, making it an essential reference for effectively managing scrutiny, assessments, adjudication proceedings, and appeals under the GST regime. It emphasizes both legal interpretation and procedural strategy, ensuring readers are equipped to respond accurately and confidently to various GST-related challenges.

- The content spans the full spectrum of GST dispute resolution and compliance handling, including:

• Detailed discussion on GST notices and their legal implications

• Practical guidance on replying to notices and handling departmental communication

• Scrutiny of returns and related procedures

• Assessment mechanisms under GST law

• Adjudication processes and principles

• Appeals before appellate authorities and higher forums

• Analysis supported by relevant case laws and judicial decisions - This edition is particularly suitable for:

• GST practitioners, consultants, and tax professionals handling litigation and compliance

• Chartered accountants, cost accountants, and company secretaries

• Legal professionals specializing in indirect taxation

• Corporate tax and compliance officers managing GST disputes

• Students and academicians seeking a practical understanding of GST procedures - With its updated legal framework, practical insights, and comprehensive coverage, this book stands as a reliable resource for addressing and resolving GST-related notices and proceedings in the evolving regulatory landscape of 2026.

Sale!

How to handle GST Notices, Scrutiny, Assessment, Adjudication & Appeals

Original price was: ₹1,595.00.₹1,180.00Current price is: ₹1,180.00. Save 26%

Out of stock

Want to be notified when this product is back in stock?

Related products

- Sale!

Understanding Applicability of Section 43b(h) to MSMEs

Books Original price was: ₹395.00.₹336.00Current price is: ₹336.00. Save 15%Add to cart - Sale! Out of stock

The Limited Liability Partnership Act, 2008

Bare Act Original price was: ₹550.00.₹402.00Current price is: ₹402.00. Save 27%View Product - Sale! Out of stock

Understanding the Provisions of Clubbing of Income

Books Original price was: ₹695.00.₹507.00Current price is: ₹507.00. Save 27%View Product - Sale! Out of stock

The Right to Information Act, 2005

Books Original price was: ₹795.00.₹676.00Current price is: ₹676.00. Save 15%View Product

2 reviews for How to handle GST Notices, Scrutiny, Assessment, Adjudication & Appeals

There are no reviews yet.